What Is a Computerized Accounting System?

How is your company doing? Being able to answer that question requires you to know how much money you're making, which in turn requires accurate bookkeeping. Keeping accurate financial records is crucial to the success of any business, so it's important to know your options. While some firms still do their bookkeeping by hand, most firms generally have too many transactions to sustain a manual accounting system. The more complicated the financial activities of your business are, the more likely it is that you'll need a computerized accounting system to ensure effective financial reporting. Computerized accounting systems are software programs that are stored on a company's computer, network server, or remotely accessed via the Internet.

Computerized accounting systems allow you to set up income and expense accounts, such as rental or sales income, salaries, advertising expenses, and material costs. They also can be used to manage bank accounts, pay bills, and prepare budgets. Depending upon the program, some accounting systems also allow you to prepare tax documents, handle payroll, and manage project costs.

You can generally customize the software to meet the needs of your business. It's important to make sure that your staff are trained and understand how to use the system correctly so that your company can successfully use your accounting program.

Distinguish between Manual and Computerized Accounting System

manual vs computerized accounting, the financial transactions are recorded, processed, and presented to generate financial statements, that are useful to the readers, in making decisions. Traditionally, accounting is done manually, by a trained accountant, with the use of registers, account books, vouchers, etc. But with the emerging technology, nowadays, computerized accounting is in vogue, due to its accuracy, convenience, and speed.

Both manual and computerized system is based on the same principles, conventions, and concept of accounting. However, they differ only in their mechanism, in the sense that manual accounting uses pen and paper, to record transactions, whereas computerized accounting makes use of computers and the internet, to enter transactions electronically.

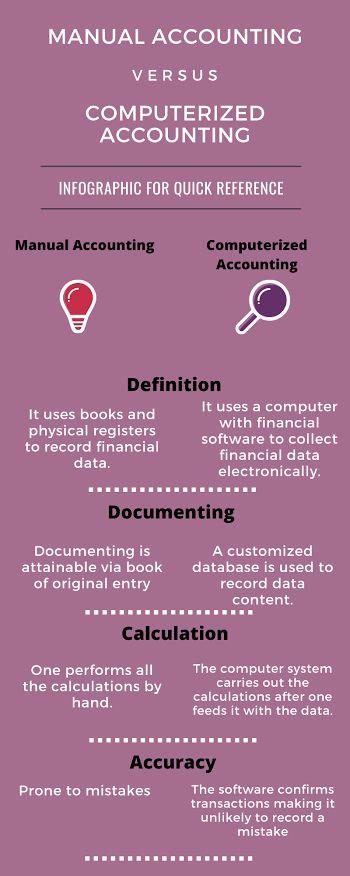

Definition of Manual Accounting

Manual Accounting, as the name signifies, is the paper-based accounting system, in which journal and ledger registers, vouchers, account books are used to store, classify and analyze financial transactions of an organization. It is often used by small businessmen, such as sole proprietors, shopkeepers, etc. to maintain the record of the business transactions, due to lower cost.

One of the advantages of the manual accounting system is its easy accessibility. It is also characterized by confidentiality, which makes sensitive information hacking free. Nevertheless, manual accounts can only be prepared correctly if the accountant possesses good knowledge of bookkeeping and accounting. Moreover, human error, such as incorrect recording of the transaction, the omission of the transaction, figure transposition, and so forth, is likely to occur while the preparation of manual accounts cannot be ignored.

Definition of Computerized Accounting

1. Computerized Accounting can be described as the accounting system that uses the computer system and pre-packaged, customized, or tailored accounting software, to keep a record of financial transactions and generate financial statements, for analysis.

2. A computerized Accounting system relies on the concept of a database. The accounting database is systematically maintained, with an active interface wherein accounting application programs and reporting systems are used.

3. Accounting framework: The framework comprises principles and a grouping structure for maintaining records.

4. Operating procedure: There is a proper procedure for operating the system so as to store and process the data.

5. Further, it requires a front-end interface, back-end database, database processing and reporting system to store data in a database-oriented application.

6. The merits of computerized accounting rely on its speed, accuracy, reliability, legibility, up-to-date information, and reports, etc.

Key Differences Between Manual and Computerized Accounting

The difference between manual and computerized accounting is explained below in points:

1. Manual Accounting refers to the accounting method in which physical registers for journals and ledger, vouchers, and account books are used to keep a record of the financial transactions. On the other hand, computerized accounting implies the method of accounting, which uses an accounting software or package, to record the monetary transactions, which happen to an organization.

2. In manual accounting, recording of the transaction can be done through the book of original entry, i.e. journal daybook. Conversely, in computerized accounting, the transactions are recorded in the form of data, in the customized database.

3. In manual accounting, all the calculations, i.e. addition, subtraction, etc. with respect to the transactions are performed manually. In contrast, in computerized accounting, there is no need to perform calculations, as the calculations are performed by the computer automatically.

4. In manual accounting, a person remains involved all the time, with the accounts, to enter and update transactions, which is tedious and time-consuming too. As against, in computerized accounting, once the transaction is entered, it is automatically updated in all the accounts to which it relates and thus, the process is comparatively faster.

5. In the manual accounting method, if there occurs an error while entering and posting the transaction in the books of accounts, then adjustment entries can be passed, for getting accurate results. Moreover, adjustment entries are also made to comply with the matching principle, i.e. the expenses of the accounting period should match the respective revenues. On the other hand, in computerized accounting, to comply with the matching principles journal and vouchers are prepared, but adjustments entries are not passed for rectification of error unless the error is an error of principle.

6. One of the merits of computerized accounting which manual accounting lacks is that in manual accounting there is no way to back up all the entries and financial statements, but in computerized accounting, the accounting records can be saved and backed up.

7. In manual accounting, the trial balance is prepared only when it is required, whereas, in computerized accounting, an instant trial balance is provided on a daily basis.

8. In a manual accounting system, the financial statement is prepared at the end of the period, i.e. financial year. On the contrary, the financial statement is provided at the click of a button, in the computerized accounting system.

Conclusion

As the number of business transactions increases, it is difficult to manage accounts manually, as it takes a lot of time to update a single transaction in all the accounts that it affects. In computerized accounting, a number of limitations of manual accounting have been removed. Whenever the transactions occur, the entry is made and it is updated automatically in all the accounts that it affects, in the computerized accounting.